Overview

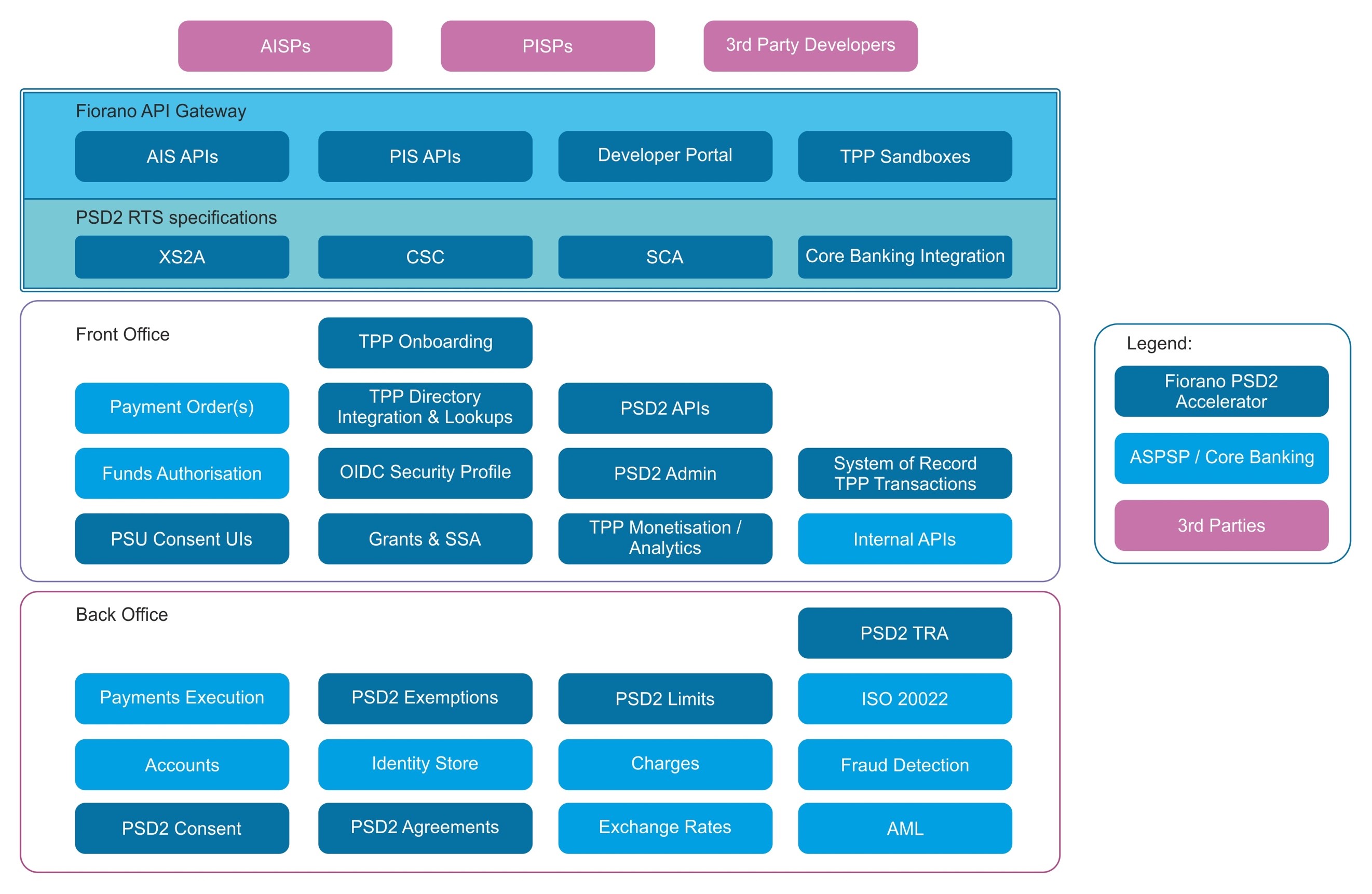

The Fiorano PSD2 Accelerator is designed to provide banks (ASPSPs in PSD2 terms) with the technology required to meet regulatory obligations, and is designed to sit along side traditional core-banking platforms, well integrated into back-office and front-office functions.